Defining New Economic Paradigms

Posted by By Akogun Akomolafe at 9 August, at 07 : 48 AM Print

Warning: count(): Parameter must be an array or an object that implements Countable in /home/alaye/public_html/wp-content/themes/Video/single_blog.php on line 56

“We have made a mistake to choose money, something which we do not have, to be our major instrument of development. We are mistaken when we imagine that we shall get money from foreign countries ‑ firstly, because to say the truth we cannot get enough money for our development, and, secondly, because even if we could get it such complete dependence on outside help would have endangered our independence and the other policies of our country.” ‑ The Arusha Declaration.

Many African patriots including the eminent Nigerian Economists, Professor Adebayo Adedeji, warned African leaders against accepting World Bank and IMF prescriptions in their quest for economic development. Many of our arguments were cogent, patriotic and well-founded on basic economic facts.

Professor Adedeji labored hard to produce a Comprehensive and Holistic Economic Plan which he called ‘An Alternative to Structural Adjustment Policy.’ Sadly for us, our leaders chose to listen to their masters in London, Paris, and Washington.

The fundamental problem with many economies in Africa is the absence of any discernible structure. So, for anyone to come and talk about adjusting a non-existing structure is fraudulent, to say the least.

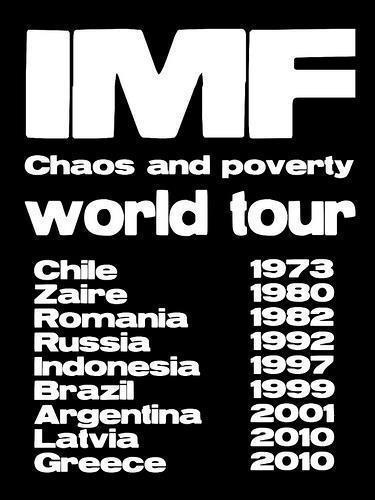

The IMF and the World Bank ruthlessly tore through African economics and left in their wake armies of unemployed (unemployable?) youth; crumbling infrastructures; devastated social services, etc, etc. The onslaught went on for about two decades before the organizations finally admitted their follies (without ever apologizing for the crimes committed against the African humanity). Africa was fed with nothing but a plethora of acronyms with SAP becoming ESAP becoming HIPC which Ghana shamelessly embraced!

The IMF and the World Bank ruthlessly tore through African economics and left in their wake armies of unemployed (unemployable?) youth; crumbling infrastructures; devastated social services, etc, etc. The onslaught went on for about two decades before the organizations finally admitted their follies (without ever apologizing for the crimes committed against the African humanity). Africa was fed with nothing but a plethora of acronyms with SAP becoming ESAP becoming HIPC which Ghana shamelessly embraced!

Few months before the spectacular collapse of global Capitalism, the ex-Chief Economist of the World Bank, Professor Joseph Stiglitz wrote a book, “Globalization and its Discontents,” in which he roundly vilified the IMF whose policies he termed ‘bad economics.’

When in the mid-1980s I was asked what I thought about the IMF proclaiming Ghana as the ‘Star Pupil’ in Africa. My reply was that if you measure economic success by the number of 4-Wheel jeeps on the roads, maybe Ghana is doing fantastic. But if we use indices such like the number of people selling dog chains on the road, the number of unemployed youth, the number of children whose parents cannot afford school fees, the number of citizens needlessly dying because they cannot pay hospital bills then Ghana is an unmitigated disaster.

The economic fundamentalists (what else to call them?) of the IMF and the World Bank have long held the high grounds by spewing economic gibberish unintelligible to the average Kwame. But as Franklin D. Roosevelt succinctly put it, “But while they prate of economic laws, men and women are starving. We must lay hold of the fact that economic laws are not made by nature. They are made by human beings.”

The meltdown of the Global Capitalist economy has revealed the apostles of Neo-liberalism for what they are: liars. The corporate media are doing their best to pull the wool over our eyes. They continue to tell outrageous lies and be engaged in pseudo analyses. The truth of the matter happened is that the Crash of 2008 happened exactly the way of the Crash of 1929/1930.

In the 1920s, greedy, amoral bankers were left unregulated and they created a bubble economy which blew in their faces resulting in misery across the globe. It required massive state intervention to correct the economic rupture caused by the unprincipled greed of the so-called financiers. Governments put tight regulation across the board to check the excesses of the bankers and these regulations were in place until the1970s. Reagan and Thatcher were the forces that removed these control in their cold pursuit of the so-called Supply-side economics.

With regulations, removed bankers were left to their own devices and they soon proved that like the Bourbon of old, they have learned nothing and forgotten nothing. They soon created another bubble economy in the mortgage and the sub-prime sectors. Japan’s bubble was the first to burst and although the lessons were there for all to see, no one seems to learn any lesson.

For those of us in Africa, we have been told many lies many times. It is time we learn the lessons of history. Our economies have been abused as experimental laboratories and we have seen the result in stunted economic growth all across Africa especially in the manufacturing and the non-extractive sectors.

Let us examine, albeit briefly, the lies (yes, lies) we have been told over the years and then consider some of the things we can do to improve our economic situation.

1. The Devaluation Lie – Devaluation is defined as the process of reducing the exchange value of a currency. For years, the lie has been told that devaluation is a huge booster to our economy. How this could be so, no one bothered to tell us. Occasionally, devaluation is used in manufacturing economy to boost export, when it is deemed that the currency is believed to be too strong against those of its trading partners. Even for middle economies (i.e. China and Malaysia) devaluation could also help in boosting exports. They could do this because they have a strong advantage in having relatively cheap labor.

But for a raw material producing nation like Ghana with virtually no industrial capacity whatever, devaluation cannot help the economy in any tangible way. First of all, we have no control (not even a say) in the pricing of our commodities. These are set in London and New York and are usually quoted in US Dollars or Euros. Devaluing our cedis has no bearing whatever on the forces that determine the prices of say, Cocoa. Devaluation for us means that we are getting less money for our Cocoa and paying more for the thing we buy from outside – which is virtually everything we consume, both domestically and industrially.

Another important factor often overlooked is that our external debts are quoted in dollars, and any devaluation is adding to our debt burden. How? Again simple logic suggests that we need more local products to service the same amount of debt. Do you still wonder why Africa’s debt is forever ballooning, despite (or is it in spite?) of all the repayments, re-scheduling?

2. The Deregulation Lie – Economics 101 teaches the Theory of Comparative Advantage whereby each nation produces what it is best suited for. This is often cited as a case for Trade Liberalization aka deregulation. Trade Deregulation will be a good idea if every country allows the free flow of trade. Alas, this is not the case, as any child knows.

The Western Countries, shouting the loudest about Free Trade, are the worst offenders when it comes to raising trade barriers to protect their economic interests. European and American farmers and farm-products exporters receive wide arrays of government subsidies. The Asians are no better – Japan has an impressive array of bureaucratic roadblocks in place to safeguard her agriculture and agro-industries. Ditto China; ditto South Korea.

It is only in Africa that we believe those who do not practice what they preach and continue to believe that our economic future could be left to the whims and caprices of a mirage called market. Deregulation can and has killed the little infant industries that we have with its attendant high rate of unemployment.

3. The Privatization Lie. Someone has, correctly, pointed out that the presumptive institutional superiority of private over public enterprises has no theoretical basis. Sadly, this has not dissuaded African governments from embarking on the fire sales of our national patrimony.

Since our local capitalists lacked the capital to buy these enterprises, it means that our national assets are being stripped and sold to foreign interests mostly Western multi-nationals as recently happened when Ghana Telecom was sold to a Dutch subsidiary of Vodafone. Even the United States, the home of the economic fundamentalists have industries that are considered ‘strategic’ and are ‘no go’ areas for foreigners yet we sold a strategic asset like GT for peanuts.

4. The Tight Credit Policy Lie. Those who came to lecture us believe in the sanctity of tight credit policy. This, they believe improves the macroeconomic performance. This is another fallacy.

In the short term, a tight credit policy might help control inflation but, in the long run, it does severe harm to the economy. How do you run a company or a national economy without money or with money available only at exorbitant rates?

Tight credit policy invariably leads to inflation. It also leads to a loss of investment and production. It distorts the economy simply because only speculators, drug pushers, and commercial activists can afford to borrow money at the rate the banks are demanding.

We all see that among the first thing the capitalist nations did was to pump money into their economies, yet we continue to listen to their lies.

The Interest Rates Lie – The Liars from the Bretton Wood institutions always call for higher interest rates in order, they say, to boost savings. The question is thus provoked: How do you save, when you are not earning, or, if as pointed out supra, SAP programmes are inflation-inducing, why save in an inflation-ridden economy?

High-interest rates discourage investment and production because there is hardly a genuine business one can one do to realize the twenty plus percent interest rate the banks are demanding. What can you produce and sell in today’s Ghana and still make enough money to pay the twenty+ percent interest rates the lending banks are demanding? Not selling even gold yield that amount of returns!

High-interest rate encourages speculation, thus deepening the dependency of our economy on foreign inputs. Speculation raises the demand for foreign currencies, further accelerating the devaluation of our currency. Do you still wonder why the Cedi is sinking?

We also have to ask: In an economy with a very high rate of unemployment, who do this economic fundamentalist expects to save? The poor are too poor to save and the noveaux rich are into lives of wanton consumption and, of course, they do not save their monies in the badly eroded local currency. No sir, it is strictly hard currency for them.

Again whenever their economies are in trouble we see Western government hurrying to reduce their interest rates to spur investment and consumption. Yet, they keep telling us that a low-interest rate is not good for our economies. In order to stimulate their production, we have also seen many of them pressing their money presses into a higher gear. This is antithetical to what they have been preaching to us over the years.

The question SAP apologists failed to answer is for whose benefits are economic policies made? What is the point of having robust macroeconomic indices when the majority of our people are impoverished? What is the point of having high economic growth rate when most of our people are badly malnourished, with no access to food, good shelter, education, and quality health? Where is the sense in having two digits growth rate when our unemployment rates cry to high heaven and many of our children are selling dog-chains and iced-water in the sun?

African leaders and elite have listened to Western advice for far too long, it is time they sat down and started asking themselves some hard questions. The economic chart they have faithfully followed for two decades has obviously failed. It is time they started constructing new, original economic paradigms to lift us from the economic morass we have been for so long.

They have to start from some basic assumptions and one of these is that since no one came into this world with a single pesewa, it follows that everyone has to create his or her own wealth. The second assumption follows from the first; no nation began life as a rich, developed country. Every single nation we today call developed built their wealth literally and figuratively from scratch. Another assumption we have to make is that economics is not a science. As the eminent economist, John Kenneth Galbraith puts it; “In economics, hope and faith coexist with great scientific pretension and also a deep desire for respectability.” Or, as H. G. Wells put it in ‘A Modern Utopia, “The science hangs like a gathering fog in a valley, a fog which begins nowhere and goes nowhere, an incidental, unmeaning inconvenience to passers-by.”

Whatever the pretensions, economics is an art and as we know that every form of art involves some gimmickry, it is time we stop regarding economic laws as some infallible scientific theorems. It is time we start to employ the same gimmickry that other nations employed to build their economics and guaranteed their people decent living. We can borrow ideas especially from US President FDR who could be credited with building modern America.

After the Great Depression when money was scarce and Americans were committing suicides in large numbers, the 32nd president of the US introduced several programmes to put Americans to work and rebuild the American economy. The new president, taking office at the height of the economic crisis, assured troubled Americans that “the only thing we have to fear is fear itself.” He acted quickly during the so-called Hundred Days (Mar.–Jan. 1933) to rush through Congress a flood of fiscal and social reform measures aimed at reviving the economy by a vast expenditure of public funds. He set up many new agencies, including the NATIONAL RECOVERY ADMINISTRATION and the PUBLIC WORKS ADMINISTRATION, to reorganize industry and agriculture under government regulation. These programs and social reforms, such as SOCIAL SECURITY, became known as the NEW DEAL.

We can cite post-war Europe as another example of economies that were grown in exact opposite to what the Bretton Woods institutions are preaching to us. The lesson we can learn is that it is fictional to preach deregulation: No single economy has been grown in the world without STRONG GOVERNMENT REGULATION. No economy has been developed by the fiction called ‘market forces.’

Nature has been very kind to us in Africa; we have among the world’s best climates. And Africa is easily the most resource-rich continent on earth. What is left is for us to harness our muscles and brains into creating the wealth to benefit us. Unless we want to be slaves to other people for eternity, we have to start thinking of ourselves first and foremost.

First and foremost we have to start producing the foods to feed ourselves. This is another lesson we can from the developed nations; they first strive to be self-sufficient in food production to guarantee themselves food-security. We have long produced the so-called cash crops that have brought us nothing but misery and mounting debt. Why do we expend our muscle in producing the things that we do not eat while spending the little money we have in importing the food we eat? This is the mother of all craziness. If we were getting fair prices for say, our cocoa, this would not be a problem as we can use the profits accruing therein to import food. But we all know that the prices of our cocoa are being manipulated to ensure that we keep living wretched lives. Common sense should tell us that we are sure losers when those to whom we are selling our products determine the prices they are going to pay while at the same time, they also determine the prices of the goods they sell to us.

Let us take agriculture for example; there is no reason why Ghana as a country should not be able to feed herself decently. President Mills recently lamented on the BBC that Ghana is spending too much money on rice importation. Why should a HIPC country with armies of unemployed youth spend 5100+ million to import rice when the cereal can be grown locally and easily too? It does not take a great brain to know that food is the first thing we need. We can become creative only when our stomachs are full.

First, we have to abandon our antiquated farming method. We should stop depending on the vagaries of nature in our agriculture. We need to build the dams and the canals to create modern Agric methods to guarantee us food security. Nay Sayers may question how where are going to pay for the dams and the canals and the irrigation projects. My retort is: How did the Americans and the Europeans and the Asians pay for theirs?

I say that until we recognize that we are in an emergency and adopt radical ideas, however unorthodox, we can get nowhere. Special Bonds, Treasury Bills are some of the economic gimmicks we can adopt for our economic development. At least we will know that we are actually developing instead of being sold the fiction that we are developing when about the only thing we are doing is being hewers of woods for the West. If President Obama is putting America in huge debt to create jobs and rebuild American infrastructures, there is no reason why we in Ghana cannot do the same. There is nothing bad, per se, in borrowing as long as it is put into productive ventures.

Another area that should demand the immediate attention of our leaders is INTEGRATION. For years we have paid lip service to integrating African economies and I say it is time to stop talking and started doing. The immortal Kwame Nkrumah and the late Cheikh Anta Diop are among great thinkers who have elucidated for us the imperatives of integrating African economies into a single, viable unit. The truth is that very few of the colonial inventions we call countries in Africa are economically viable. About thirty of the so-called independent countries are land-locked who have to import virtually everything they consume! Those who sundered our societies at Berlin clearly knew what they were doing.

Let us take currency for example. A Ghanaian that wants to buy a product from Nigeria must first buy a hard currency, which means Euro or Dollar. The same goes for a Nigerian who wants to buy a Gambian product. What this means is that each and every time Africans trade among themselves someone somewhere is making a cut. This is madness. Why should it be so? Even the developed economies of the EU countries have opted for a single currency with very few exceptions. We need a common currency, especially in the West Africa sub-region, and we need it now.

Let us buttress this with an example. Nigeria imports large quantities of salt or her petroleum industries. Ghana, on the other hand, spends a large chunk of her meager earnings in importing crude oil. Both brother countries are buying vast quantities of foreign exchange for these transactions. Who is benefiting from this ludicrous situation, certainly not the peoples of the two countries? Before the Europeans came we were bartering trades among ourselves, why do we abandon this age-old practice and saddled ourselves with huge debt owed to foreigners? Why should it be beyond the competence of our leaders to evolve a system whereby foreign exchange is totally eliminated in exchanging Nigerian oil for Ghana’s salt? I have said it somewhere that our poverty stemmed not from a poverty of money, but of ideas.

It is the time our leaders and elite stop talking theories and start talking sense. They should start to speak to us in languages in simple languages we could understand. Our President need not go to far away Great (?) Britain to seek help in rebuilding our economy. The British economy itself is in serious troubles with no one clued for a solution. Let us for once say no to the colonial masters.

“But while they prate of economic laws, men and women are starving. We must lay hold of the fact that economic laws are not made by nature. They are made by human beings.” Franklin D. Roosevelt (1882-1945), U.S. Democratic politician, president. Speech, 2 July 1932, to Democratic national convention, accepting presidential nomination.

About the Author

Femi Akomolafe is a passionate Pan-Africanist. A columnist for the Accra-based Daily Dispatch newspaper and Correspondent for the New African magazine. Femi lives in both Europe and Africa and writes regularly on Africa-related issues for various newspapers and magazines.

Femi was the producer of the FOCUS ON AFRICANS TV Interview programme for the MultiTV Station.

He is also the CEO of Alaye Dot Biz Limited Dot Biz, a Kasoa-based Multimedia organisation that specialises in Audio and Video Production. He loves to shoot and edit video documentaries.

His highly-acclaimed books (“Africa: Destroyed by the gods,” “Africa: It shall be well,” “18 African Fables & Moonlight Stories” and “Ghana: Basic Facts + More”) are now available for sales at the following bookshops/offices:

- Freedom Bookshop, near Apollo Theatre, Accra.

- The Daily Dispatch Office, Labone – Accra

- WEB Dubois Pan-African Centre, Accra

- Ghana Writers Association office, PAWA House, Roman Ridge, Accra.

- African Kitchen in Amsterdam Bijlmer

Where to buy them online:

On Lulu Books:

18 African Fables & Moonlight Stories https://goo.gl/Skohtn

Ghana: Basic Facts + More: https://goo.gl/73ni99

Africa: Destroyed by the gods: https://goo.gl/HHmFfr

Africa: It shall be well: https://goo.gl/KIMcIm

Africa: it shall be well

on Kindle books: https://www.createspace.com/4820404

on Amazon books: http://goo.gl/QeFxbl

on Lulu Books: https://goo.gl/SQeoKD

Africa: Destroyed by the gods

on Kindle books: https://www.createspace.com/4811974

on Amazon books: http://goo.gl/1z97ND

on Lulu Books: http://goo.gl/KIMcIm

My Lulu Books page: http://www.lulu.com/spotlight/FemiAkomolafe

Get free promotional materials here:

- Africa: it shall be well: http://alaye.biz/africa-it-shall-be-well-introduction-in-pdf/

A FREE Chapter of ‘Africa: It shall be well’ could be downloaded here: http://alaye.biz/africa-it-shall-be-well-a-free-chapter/

- Africa: Destroyed by the gods (How religiosity destroyed Africa) http://alaye.biz/africa-destroyed-by-the-gods-introduction/

A FREE Chapter of ‘Africa: Destroyed by the gods’ could be downloaded here: http://alaye.biz/africa-destroyed-by-the-gods-free-chapter/

Contact Femi:

Femi’s Blog: www.alaye.biz/category/blog

Website: www.alaye.biz

Femi on Amazon https://www.amazon.com/author/femiakomolafe

Twitter: www.twitter.com/ekitiparapo

Facebook:https://www.facebook.com/alayeclearsound;

Gmail+: https://plus.google.com/112798710915807967908;

LinkedIn: www.linkedin.com/in/femiakomolafe

Email: fakomolafe@gmail.com

Kindly help me share the books’ links with your friends and, grin, please purchase your copies.

Comradely,

Femi Akomolafe